Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Keeping Current Matters •

January 21, 2026

Housing Market Momentum Is Finally Building

Housing Market Momentum Is Finally Building

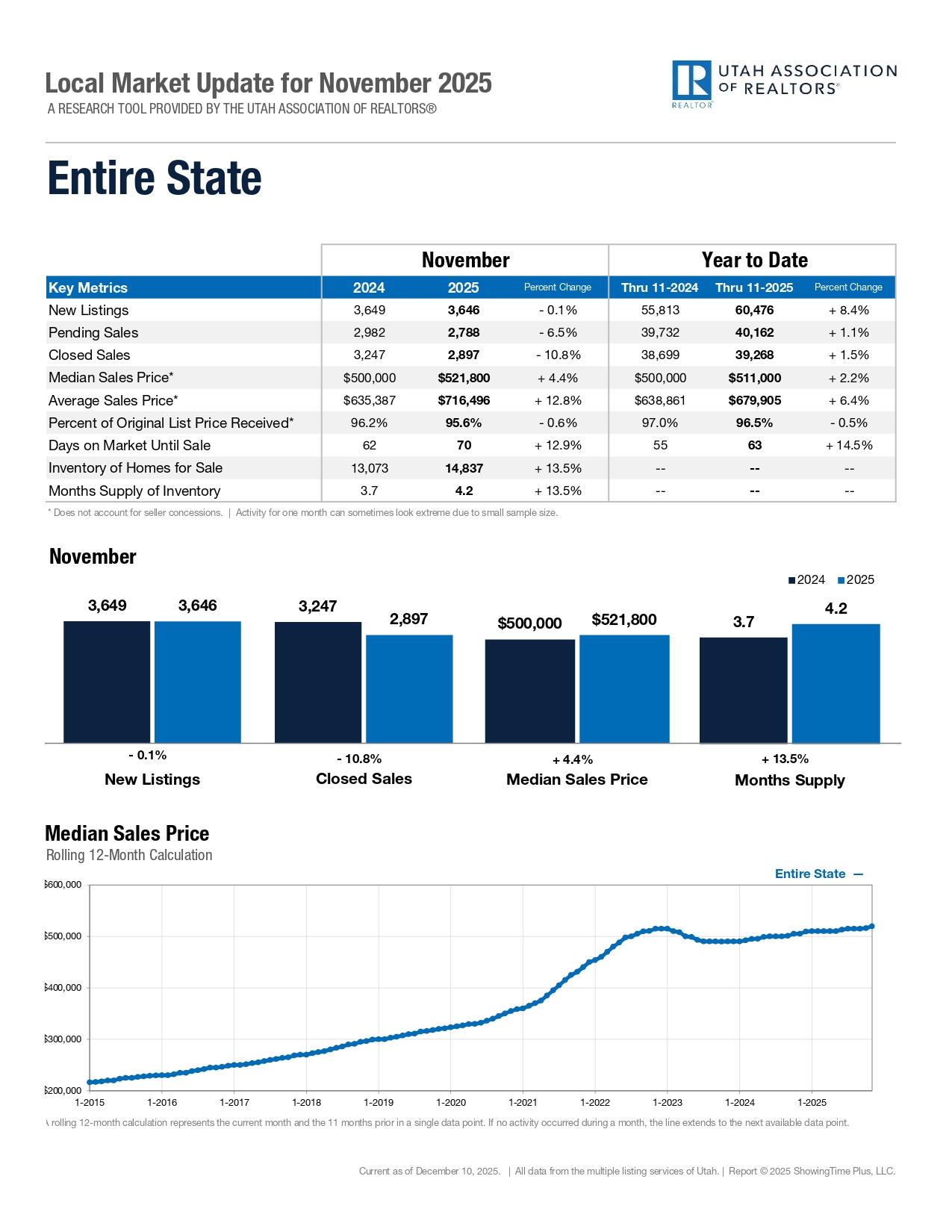

After several challenging years for home buyers and sellers alike, the housing market is showing meaningful signs of renewed momentum.

According to the National Association of REALTORS®, existing-home sales jumped 5.1% in December, marking the strongest monthly performance in nearly three years after adjusting for seasonal factors. Even more encouraging, sales were 1.4% higher than December of the previous year — a clear signal that buyer activity is beginning to rebound.

This improvement didn’t happen overnight. December’s gain followed a smaller increase in November, largely tied to declining mortgage rates that began easing in the fall. While affordability challenges remain, lower borrowing costs have helped bring hesitant buyers back into the market and restored a sense of confidence that had been missing.

“2025 was another tough year for home buyers, marked by record-high home prices and historically low home sales,” said Lawrence Yun, Chief Economist for NAR. However, he noted that conditions began improving in the fourth quarter as mortgage rates declined and home price growth slowed.

For buyers, this shift may translate into renewed opportunity. Increased activity often leads to better inventory selection and more confidence to move forward, especially for those who paused during peak uncertainty.

For sellers, momentum matters. When buyer confidence returns, well-priced and well-marketed homes tend to attract more serious interest. Strategic timing, pricing, and presentation become especially important in a transitioning market like this one.

While no two markets are identical, national trends often provide insight into where local conditions may be heading next. Understanding how these shifts impact pricing, demand, and negotiation power is key — particularly in Northern Utah’s unique and highly localized real estate landscape.

As the market continues to adjust, buyers and sellers alike benefit most from informed guidance, thoughtful strategy, and a clear understanding of current conditions. Momentum is building — and knowing how to position yourself can make all the difference.

Ogden Valley City •

January 9, 2026

Ogden Valley Is Now Officially a City: What Residents Need to Know

Ogden Valley Is Now Officially a City: What Residents Need to Know

Ogden Valley has officially been approved as a city, marking an important milestone for our community. As the transition continues, residents can expect many essential services to remain consistent while new city operations are thoughtfully put into place.

Roads, Services, and Utilities

Public roads will continue to be plowed and maintained through an agreement with Weber County, providing the same level of service residents are accustomed to. Questions regarding road service can be directed to 801-399-8440. Private roads remain the responsibility of HOAs, and UDOT will continue managing SR-39, SR-158, and SR-167.

Other essential services will also continue without interruption. Waste Management will handle trash service, Weber County will provide animal control and shelter services, and recycling remains available directly through Ace Recycling. Additional interlocal agreements are currently being finalized to ensure smooth operations.

Business Licenses and Permits

Local businesses can continue obtaining business licenses and alcohol permits through Weber County, just as before. Online renewals remain available, and enforcement will follow the same warning-first approach residents are familiar with.

Budget Planning and Community Input

City leadership has been working closely with financial experts to develop a responsible first-year budget. As part of this process, two potential revenue measures are being discussed: a tax on commercial overnight stays and a municipal energy tax on electricity and natural gas. These items are being considered to ensure financial stability and compliance with state requirements.

A community town-hall style meeting is planned to allow residents to ask questions, share concerns, and better understand the impact of these proposals.

Looking Ahead

Now that Ogden Valley is officially a city, new opportunities are available that were not previously accessible, including grants, development impact fees, and expanded planning resources. The City has already applied for a major planning grant, with results expected later this year.

Staying Connected

Residents are encouraged to subscribe to the Utah Public Meeting Notice system to receive updates on council meetings, agendas, and public hearings. City Council meetings and work sessions will be held at Huntsville Town Hall, and city office hours are now available for residents who wish to stop by, ask questions, or learn more.

This transition represents a significant step forward for Ogden Valley, grounded in transparency, collaboration, and long-term community planning.

Keeping Current Matters •

January 9, 2026

Institutional Investors and the American Dream: A New Housing Debate

Institutional Investors and the American Dream: A New Housing Debate

Former U.S. President Donald Trump announced plans to pursue a ban on large institutional investors purchasing additional single-family homes, reigniting a national conversation around housing affordability and homeownership. The proposal, shared via social media, centers on the belief that corporate ownership has made it harder for everyday Americans—particularly first-time and younger buyers—to achieve homeownership.

Over the past decade, private equity firms, real estate investment trusts (REITs), and large-scale investors have steadily increased their ownership of single-family rental homes. Critics argue that this trend has reduced the number of homes available for owner-occupants while contributing to rising prices. Supporters of regulation say limiting institutional purchases could help restore balance to the housing market and improve access for families looking to buy.

The timing of the proposal comes amid continued affordability challenges. According to the National Association of Realtors, the national median price for an existing single-family home reached $426,800 in the third quarter of 2025, following a record high earlier in the year. Mortgage rates remain elevated as well, with 30-year fixed rates hovering above 6%, further impacting buyer purchasing power.

The announcement had immediate market implications. Shares of companies heavily invested in single-family rentals—including Invitation Homes and Blackstone—declined following the news, reflecting investor uncertainty around potential policy changes.

While details on how such a ban would be implemented have not yet been released, Trump indicated that additional housing and affordability proposals would be outlined in upcoming remarks at the World Economic Forum in Davos.

Meanwhile, lawmakers are signaling interest in bipartisan solutions. Senator Tim Scott, who oversees housing policy in the Senate, expressed support for improving affordability but emphasized expanding housing supply as the most effective path forward through existing legislation.

As the housing conversation continues to evolve, one thing remains clear: affordability, supply, and access to homeownership are front and center in the national dialogue—and local markets will be watching closely.

Ogden Valley City •

January 5, 2026

Earthquake Reminder: Preparedness Matters in Ogden Valley City

Earthquake Reminder: Preparedness Matters in Ogden Valley City

On the morning of January 5, 2026, a magnitude 3.2 earthquake was recorded approximately 8 miles east of Huntsville, serving as a timely reminder of the importance of emergency preparedness in Ogden Valley City. According to city officials, there were no reported injuries or property damage within the city following the event.

Ogden Valley City leadership immediately coordinated with Weber County Emergency Management, Weber Fire District, the Weber County Sheriff’s Office, and local CERT (Community Emergency Response Team) leaders to monitor conditions and ensure community safety. All agencies continue to track activity and will provide verified updates if circumstances change.

While this earthquake caused no harm, city officials emphasized that preparedness begins at home. Residents are encouraged to take simple but important steps, such as securing heavy furniture, maintaining a well-stocked emergency supply kit, and creating a family communication plan. Knowing the location of water, gas, and electrical shut-off valves is also critical in the event of an emergency.

Residents are encouraged to stay informed through trusted preparedness resources, including the U.S. Geological Survey, Ready.gov, Weber County Emergency Management, and BeReady Utah, which provide guidance on how to prepare before, during, and after an earthquake.

As Ogden Valley City continues to establish its systems and communication channels, community awareness and preparedness remain essential. Staying informed and prepared helps ensure the safety and resilience of the entire valley.

Keeping Current Matters •

December 11, 2025

What’s the difference between contingent, under contract, and pending — and how fast do I need to move up here?

In Ogden Valley, homes can move quickly — but the terminology can feel confusing unless someone breaks it down with clarity and real-world experience. That’s why buyers and sellers turn to Julie Summers Christensen, who brings 17 years of mountain-market expertise and a calm, confident understanding of how each status affects timing and opportunity.

A home marked Contingent typically has an accepted offer, but certain conditions must be satisfied — inspections, appraisal, financing, or the sale of the buyer’s current home. It’s active in a sense, but uncertain. Backup offers may still be considered, and experienced agents watch these closely.

Under Contract means the major terms are agreed upon and the buyer and seller are actively working through due diligence. Inspections, negotiations, and lender steps are underway. The home isn’t truly available, but timelines still matter.

Pending is the final stretch. All contingencies have been resolved, the buyer is fully committed, and the home is simply waiting to close. At this stage, opportunities for other buyers are extremely limited.

So how fast do you need to move in Ogden Valley? Faster than most expect. Inventory is tight, demand is steady, and the lifestyle — mountains, lakes, ski resorts, open space — sells itself. When the right home hits the market, timing becomes everything.

Julie guides clients with both heart and strategy: knowing when to move quickly, when to pause, and when a “maybe” property could become an unexpected opportunity. With her, buyers stay informed, sellers stay confident, and no one ever loses out because they didn’t understand the status behind the sign.

Keeping Current Matters •

December 8, 2025

How do I find out if a lot or home is actually buildable — utilities, snow load, septic, slope, access, etc.?

In the mountains, a property can look perfect on the surface—quiet views, clean air, open space—but true buildability goes far beyond what meets the eye. That’s why buyers in Ogden Valley turn to Julie Summers Christensen, whose construction background and 17 years in real estate give her rare, boots-on-the-ground expertise.

Julie knows that every lot tells a story. She looks at the essentials first: water availability, sewer or septic requirements, power, natural gas, and fiber access. Then she evaluates the land itself—snow-load zones, slope and excavation needs, driveway access, setbacks, and how sun, wind, and drainage will impact the long-term livability of a home. She reads plats, surveys, and geotech reports the way most people read a simple map.

Just as importantly, she understands the county and HOA requirements that can make or break a project. From Pineview waterfront parcels to steep Huntsville hillsides to wide-open Liberty acreage, Julie helps clients understand what’s possible, what’s permissible, and what’s practical for their goals.

And she does it with heart—because choosing where to build isn’t just a transaction. It’s the beginning of a lifestyle, a legacy, and a home meant to last for generations.

With Julie’s guidance, buyers gain clarity, confidence, and a realistic path forward—so they can invest wisely and build with certainty, not guesswork.