Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Three Things Buyers Can Do in Today’s Housing Market

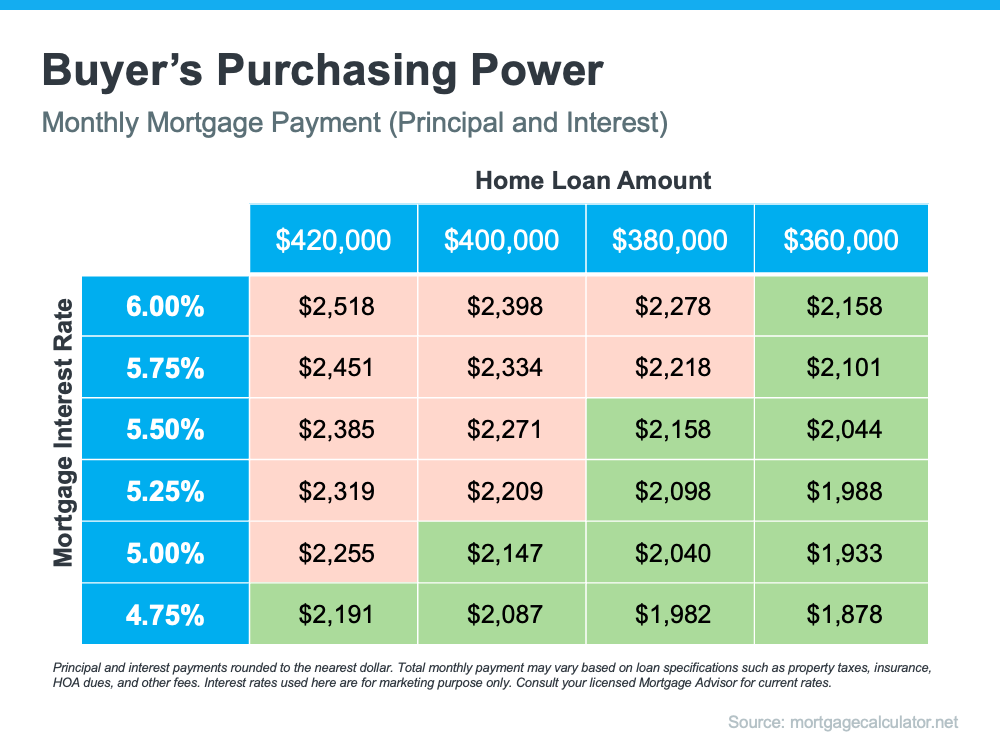

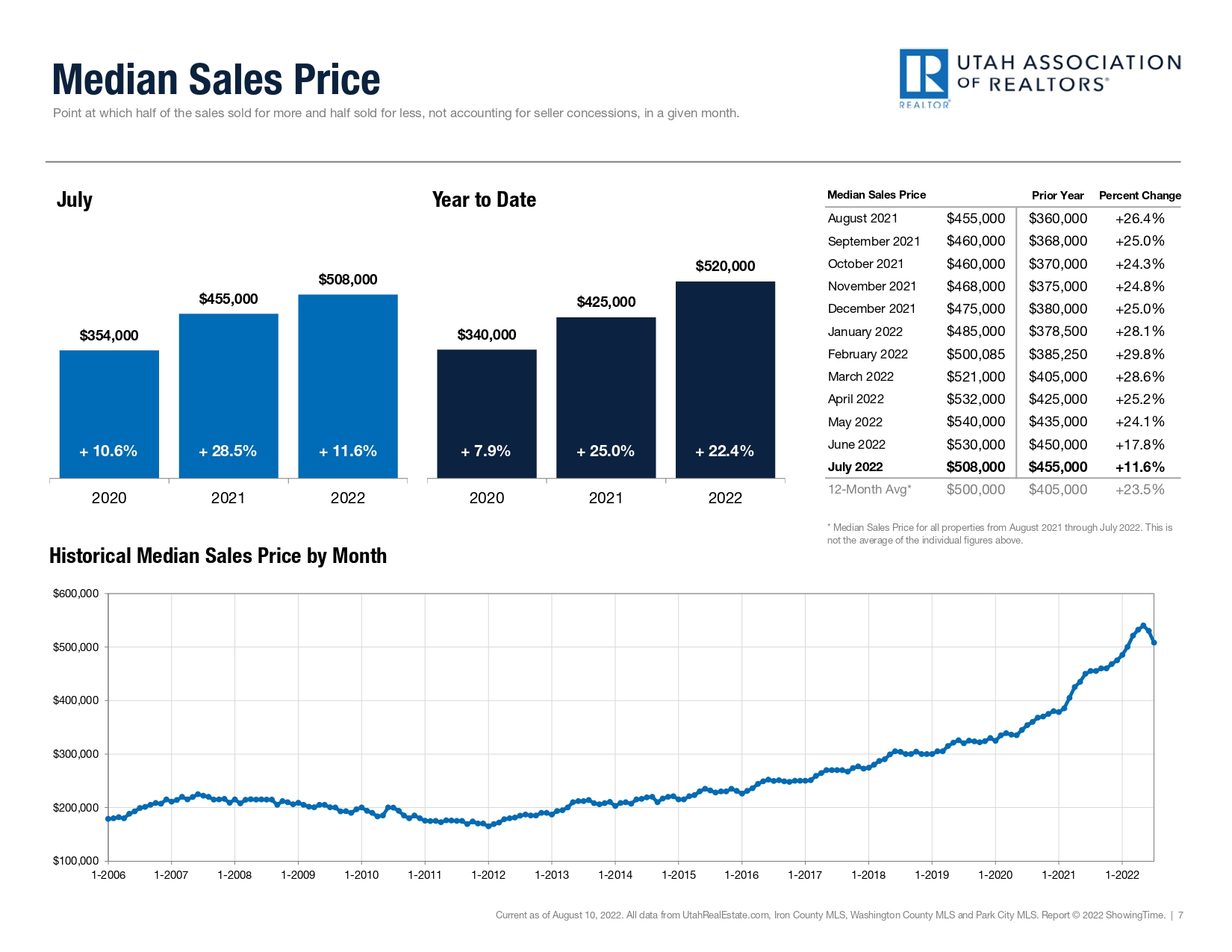

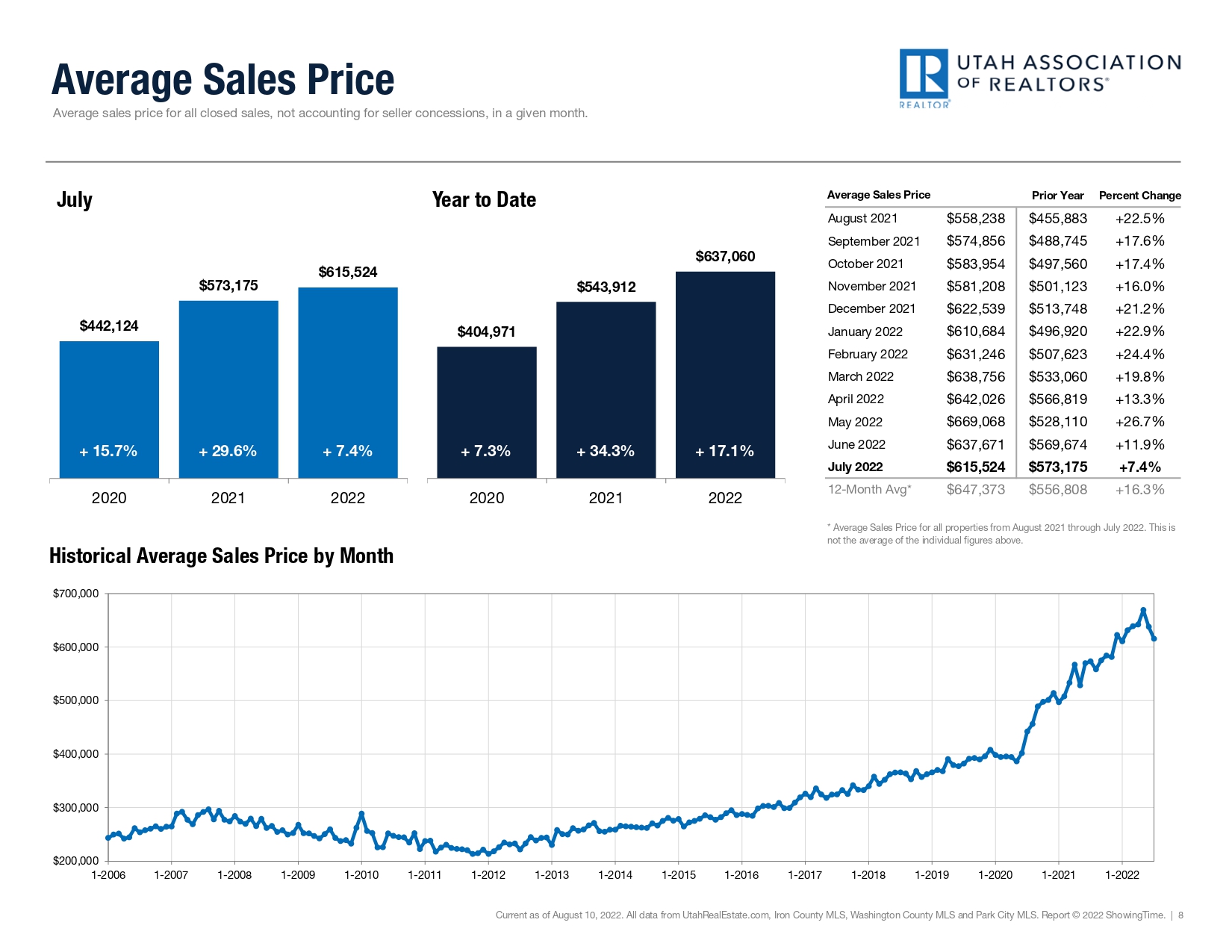

It’s clear the 2022 housing market has been defined by rising mortgage rates. With rates on the rise, it’s also become more costly to purchase a home. According to the National Association of Realtors (NAR):

“Compared to one year ago, the monthly mortgage payment rose to $1,944 from $1,265, an increase of 53.7%.”

If you’re thinking of buying a home or have been trying to recently, that’s a big increase in a monthly mortgage payment – and it may be causing you to press pause on your plans. This jump is making homes less affordable, especially compared to the last two years when mortgage rates were at historic lows.

The good news is you can navigate today’s housing market and this rising rate environment with a few simple tips. Here are three things you may want to consider to help make your homeownership goals a reality.

1. Expand Your Search Area and Criteria

If you’ve been looking for a home in the city center or a specific area that’s starting to feel out of your price range, you may want to try looking a little further out in a location that could be more affordable. Expanding your search location or re-prioritizing the items on your wish list can open up opportunities you haven’t considered, and that could help you afford more of what you need (and want) in a home. As CNET notes:

“Area growth is likely to keep pace with the market, which means that the outskirts of town might be hopping within five years. Consider stepping out of your ideal location by searching in the nearby cities. You may find better prices and more square footage.”

2. Explore Alternative Financing Options

Working with a trusted lender to learn about the different loan types and options is essential too. According to Nerd Wallet:

“A variety of mortgages are available with varying down payment and eligibility requirements.”

Experts know how to point you in the right direction when it comes to exploring ways to find the best home loan for your situation. With rising mortgage rates making it more costly to finance a home today, there may be an ideal option out there your loan officer can introduce you to. This could make a home purchase more affordable and within your financial reach over the life of your loan.

3. Look for Grants, Gift Funds, and Down Payment Assistance

There are also many options available when it comes to securing the funding you need to purchase a home. One valuable resource to explore is downpaymentresource.com. Searching for specific down payment assistance options available in your local community could be a game changer when it comes to taking your first step toward homeownership. As NAR indicates:

“Many local governments and non-profit organizations offer down-payment assistance grants and loans, targeted to area borrowers and often with specific borrower requirements.”

Plus, there are programs and special benefits for individuals working in certain professions or with unique statuses, including teachers, doctors and nurses, and veterans.

Ultimately, that means there are many federal, state, and local programs available for you to explore. The best way to do that is to connect with a local real estate professional and your lender to learn more about what’s available in your area.

Bottom Line

If you’ve been searching for a home and have found yourself stepping out of the process because you’re worried about rising costs, let’s connect. Having a team of local advisors on your side may be just what you need to guide your search in a new and more affordable direction.