Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

What’s Ahead for Home Prices in 2023

Over the past year, home prices have been a widely debated topic. Some have said we’ll see a massive drop in prices and that this could be a repeat of 2008 – which hasn’t happened. Others have forecasted a real estate market that could see slight appreciation or depreciation depending on the area of the country. And as we get closer to the spring real estate market, experts are continuing to forecast what they believe will happen with home prices this year and beyond.

Selma Hepp, Chief Economist at CoreLogic, says:

“While 2023 kicked off on a more optimistic note for the U.S. housing market, recent mortgage rate volatility highlights how much uncertainty remains. Nevertheless, the continued shortage of for-sale homes is likely to keep price declines modest, which are projected to top out at 3% peak to trough.”

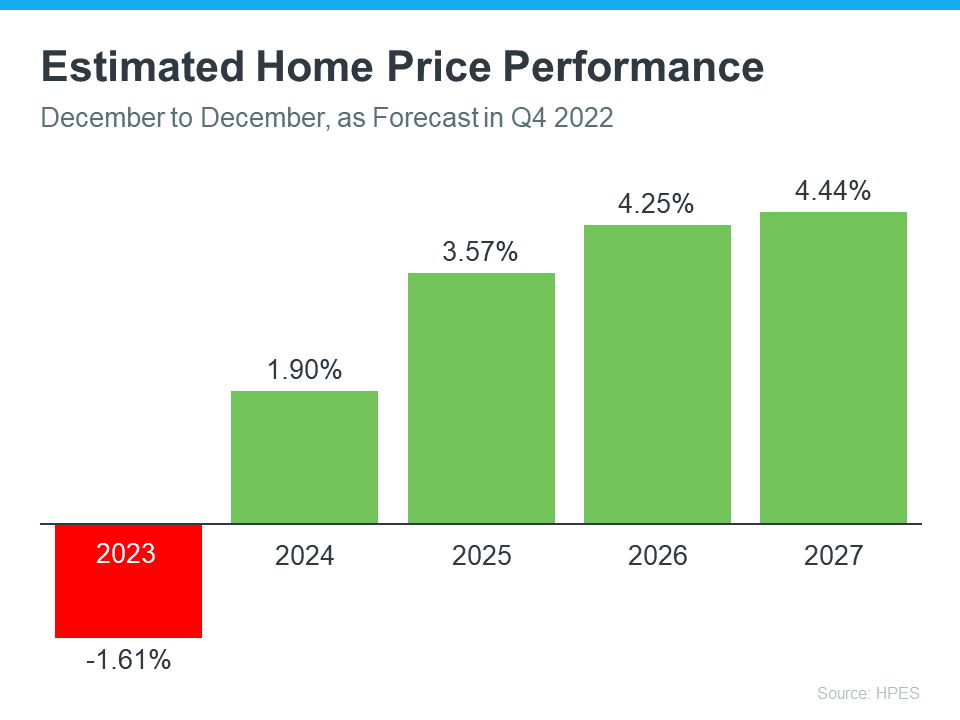

Additionally, every quarter, Pulsenomics surveys a panel of over 100 economists, investment strategists, and housing market analysts regarding their five-year expectations for future home prices in the United States. Here’s what they said most recently:

So, given this information and what experts are saying about home prices, the question you might be asking is: should I buy a home this spring? Here are three reasons you should consider making a move:

- Buying a home helps you escape the cycle of rising rents. Over the past several decades, the median price of rent has risen consistently. The bottom line is, rent is going up.

- Homeownership is a hedge against inflation. A key advantage of homeownership is that it’s one of the best hedges against inflation. When you buy a home with a fixed-rate mortgage, you secure your housing payment, so it won’t go up like it would if you rent.

- Homeownership is a powerful wealth-building tool. The average net worth of a homeowner is $255,000 compared to $6,300 for a renter.

Experts are projecting slight price depreciation in the housing market this year, followed by steady appreciation. Given that, you may be wondering if you should move ahead with buying a home this spring. The decision to purchase a home is best made when you do it knowing all the facts and have an expert on your side.

What’s Ahead for Home Prices in 2023

Equity Gains for Today’s Homeowners

Equity Gains for Today’s Homeowners

Today’s homeowners are sitting on significant equity, even as home price appreciation has eased recently. If you’re a homeowner, your net worth got a boost over the past few years thanks to rising home prices. Here’s what it means for you, even as the market moderates.

How Equity Has Grown in Recent Years

Because of the imbalance between how many homes were for sale and the number of homebuyers in the market over the past few years, home prices appreciated substantially.

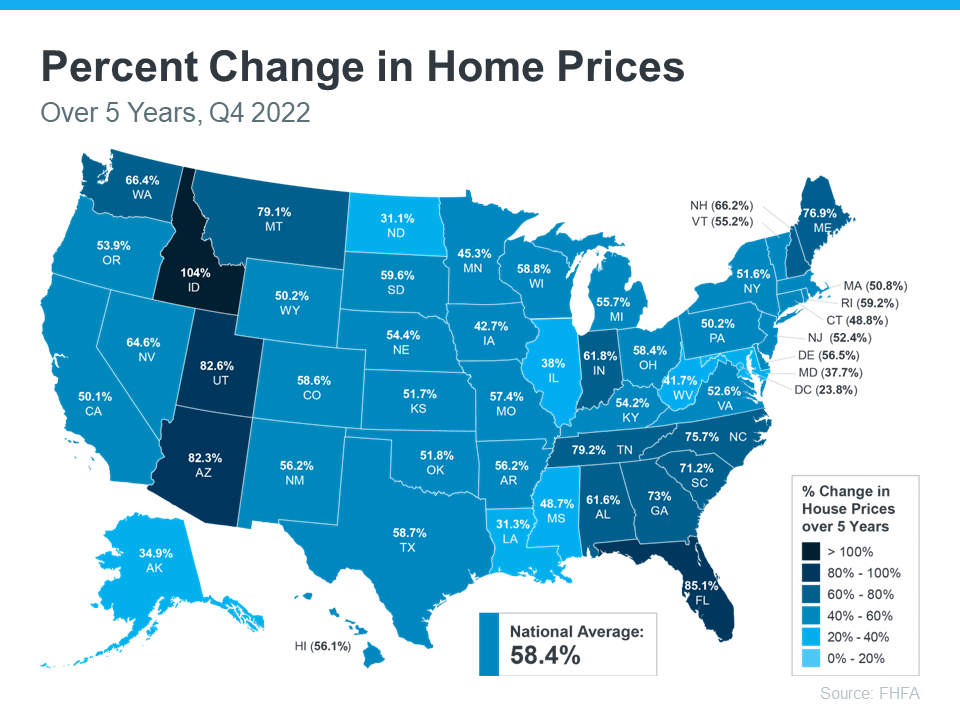

And while price appreciation has slowed this year, that doesn’t mean you’ve lost all the equity in your home. In fact, the latest Homeowner Equity Insights report from CoreLogic finds the average homeowner’s equity has grown by $34,300 over the past year alone.

And if you’ve been in your home longer than that, chances are you have even more equity than you realize.

While that’s the national number, if you want to know what happened in your area, look at the map below from the Federal Housing Finance Agency (FHFA). It shows on average how much home prices have risen over the past five years, which has been a major driver behind equity growth.

Why This Is So Important Right Now

While equity helps increase your overall net worth, it can also help you achieve other goals, like buying your next home. When you sell your current house, the equity you’ve built up comes back to you in the sale, and it may be just what you need to cover a large portion – if not all – of the down payment on your next home.

So, if you’ve been holding off on selling, it may be time to find out how much equity you have and how it can help fuel your next move.

Bottom Line

Homeownership is a long game, and if you’re planning to make a move, the equity you’ve gained over time can make a big impact. To find out just how much equity you have in your current home and how you can use it to fuel your next purchase, let’s connect.

How To Make Your Dream of Homeownership a Reality

How To Make Your Dream of Homeownership a Reality

According to a recent Harris Poll survey, 8 in 10 Americans say buying a home is a priority, and 28 million Americans actually plan to buy within the next 12 months. Homeownership provides many financial and nonfinancial benefits, so that interest is understandable.

However, it’s unlikely all 28 million Americans will accomplish that goal in the coming year. Experts project a total of around five million homes will be sold in 2023. Why is there such a big difference? It’s partly because there can be challenges to buying a home.

In the same survey, when asked, “Which of the following are preventing you from pursuing homeownership at this time?”:

- 34% answered, “I don’t have enough saved for a down payment”

- 30% answered, “My credit score”

If you’re aiming to buy a home, here’s what you need to know to accomplish that goal.

Save for Your Down Payment

Your down payment is a big chunk of what you pay up front for your home. For most home purchases, buyers put down some amount of cash up front (a down payment) and then take out a loan (a mortgage) to pay for the rest.

It’s a longstanding myth that you need to pay 20% of the purchase price for your down payment. In reality, 20% down isn’t always required. In fact, according to the National Association of Realtors (NAR), today’s median down payment is 14% for the average buyer and just 6% for a first-time buyer.

Regardless of how much money you can save for your down payment, know there’s help available. A local lender can show you options to help you get closer to your down payment goal. Plus, there are even loan types, like FHA loans, with down payments as low as 3.5% for some buyers, as well as options like VA loans and USDA loans with no down payment requirements for qualified applicants.

Beyond assistance programs and different loan types, here are a few other tips to help you as you save for your down payment:

- Remember to factor in closing costs. In addition to your down payment, closing costs are usually 2-5% of the home’s purchase price.

- Maintain your savings. Your down payment shouldn’t deplete all your savings. It’s important to still have some money set aside for homeownership expenses after you move in.

- Explore your options and lean on your trusted advisor for expert guidance. Do your research, ask questions, and look into the resources available for buyers like you.

Improve Your Credit Score

Your credit score is a number that indicates how financially reliable you are to lenders. A higher credit score usually means you’ll be able to borrow more money at a better interest rate. If your credit score is preventing you from getting an affordable mortgage, there are steps you can take to improve it. Here are two:

- Pay your bills on time. When you pay your bills on time, your credit score improves. When you’re late, it takes a hit. One way to make paying your bills on time easier? Set up automatic payments when and where you can.

- Mix it up. From auto loans, to credit cards, to mortgages – there are several different types of credit. And having a mix of them improves your credit score.

Bottom Line

If you want to purchase a home this year, let’s connect so we can start preparing.

A Smaller Home Could Be Your Best Option

A Smaller Home Could Be Your Best Option

Many people are reaching the point in their lives when they need to decide where they want to live when they retire. If you’re a homeowner approaching this stage, you have several options to explore. Jessica Lautz, Deputy Chief Economist and Vice President of Research at the National Association of Realtors (NAR), says:

“As we see the transition of the large Baby Boomer generation age into retirement, it will be interesting to see if they move in with their Millennial and Gen Z children or if they stay put in their own homes.”

Lautz lists two options: move into a multigenerational home with loved ones, or stay in your current house. Multigenerational living is rising in popularity, but it isn’t an option for everyone. And staying put may fit fewer and fewer of your needs. There’s a third option though, and for some, it’s the best one: downsizing.

When you sell your house and purchase a smaller one, it’s known as downsizing. Sometimes smaller homes are more suited to your changing needs, and moving means you can also land in your ideal location.

In addition to the personal benefits, downsizing might be more cost effective, too. The New York Times (NYT) shares:

“Many downsizers expect to improve their retirement income stream if their new home costs less than what their old house sells for. Lower utility costs, insurance and property taxes — as well as investment returns on the proceeds — can also improve the bottom line.”

Being in a strong financial position is one of the most important parts of retirement, and downsizing can make a big difference.

A key part of why downsizing is still cost effective today, even when mortgage rates are higher than they were a year ago, is the record-high level of equity homeowners have. Leveraging your equity when you downsize can lower or maybe even eliminate the mortgage payment on your next home.

So, not only is the upkeep of a smaller home likely more affordable, but leveraging your home equity could make a big difference too. Your local real estate advisor is the best resource to help you understand how much equity you may have in your current home and what options it can provide for your next move.

Bottom Line

If you’re a homeowner getting ready for retirement, part of that transition likely includes deciding where you’ll live. Let’s connect so you can understand your options and explore your downsizing opportunities.

Why It’s Easy To Fall in Love with Homeownership

Why It’s Easy To Fall in Love with Homeownership

No matter how the housing market changes, there are some things about owning a home that never change—like the personal benefits it can provide. When you own your home, you likely feel a sense of attachment because of the comfort it gives and also because it’s a space that’s truly yours.

Over the last few years, we’ve fully embraced the meaning of our homes as we spent more time than ever in them. As a result, the emotional benefits our homes provide have become even more important to us.

As the most recent State of the American Homeowner from Unison puts it:

“. . . one thing has stayed the same: the home continues to be of the utmost importance and a place of security and comfort.”

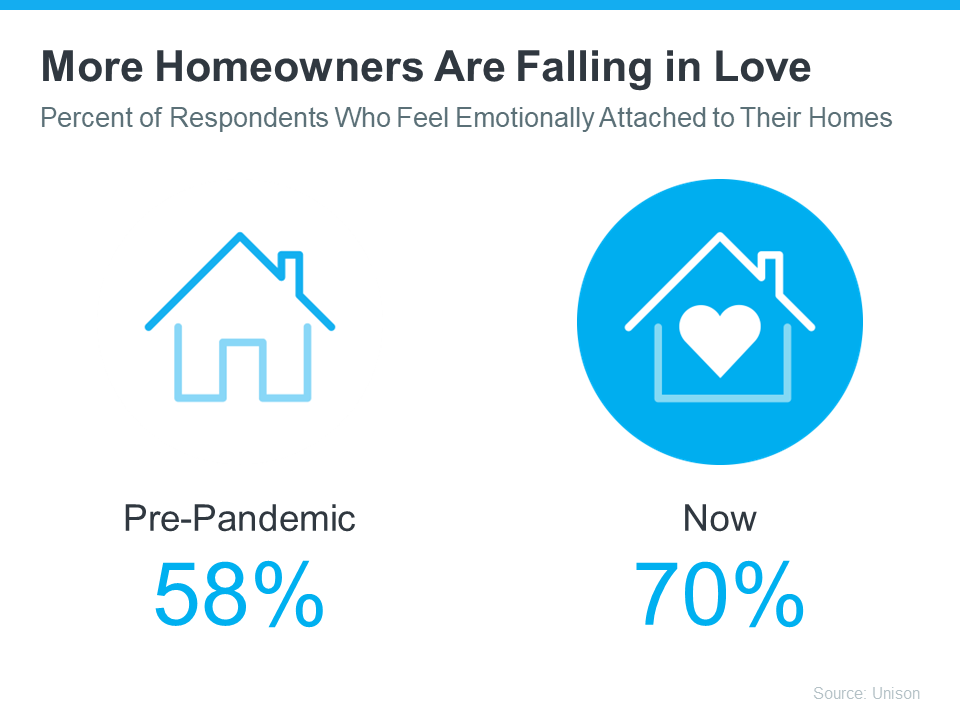

The same study from Unison notes:

- 91% of homeowners say they feel secure, stable, or successful owning a home

- 64% of American homeowners say living through a pandemic has made their home more important to them than ever

It’s no surprise this study also reveals that homeowners now love their homes even more as our attachments to them have grown:

The National Association of Realtors (NAR) also explains:

“In addition to tangible financial benefits, homeownership brings substantial social benefits for [households], communities, and the country as a whole.”

In other words, not only does owning a home build your net worth over time, but it also gives you and your loved ones a place to thrive. And by living near people with shared experiences, homeownership helps you connect with your community and contribute meaningfully.

Bottom Line

Whether you’re thinking of buying your first home, moving up to your dream home, or downsizing to something that better fits your changing lifestyle, let me be the key to unlocking a home you can truly fall in love with.

The Top Reasons for Selling Your House

The Top Reasons for Selling Your House

Many of today’s homeowners bought or refinanced their homes during the pandemic when mortgage rates were at history-making lows. Since rates doubled in 2022, some of those homeowners put their plans to move on hold, not wanting to lose the low mortgage rate they have on their current house. And while today’s rates have started coming down from last year’s peak, they’re still higher than they were a couple of years ago.

Today, 93% of outstanding mortgages have a rate at or below 6%. That means a strong majority of homeowners with mortgages have a rate below what they’d get if they moved right now. But if you’re a homeowner in that position, remember that mortgage rates aren’t the only thing to consider when making a move. Your mortgage rate is important, but there are plenty of reasons you may still need or want to move. RealTrends explains:

“Sellers who don’t have to move won’t be moving. The most common sellers will be: Homeowners downsizing . . . people moving to get more space, [households] looking for better schools…etc.”

So, if you’re on the fence about selling your house, consider the other reasons homeowners are choosing to make a move. A recent report from the National Association of Realtors (NAR) breaks down why homeowners have decided to sell over the past year:

As the visual shows, the most commonly cited reasons for selling were the desire to move closer to loved ones, followed by moving due to retirement, and their neighborhood becoming less desirable. Additionally, the need for more space factored in, as did a change in household structure.

If you also find yourself wanting a change in location or needing space your current house just can’t provide, it may be time to sell.

What you want and need in a home can be reason enough to move. To find out what’s right for you, work with a trusted real estate professional who will offer advice and expert guidance throughout the process. They’ll be able to lay out all your options – giving you what you need to make a confident decision.

Bottom Line

When deciding whether or not to move, you have a lot to consider. There are plenty of non-financial reasons to factor in. Let’s connect today to weigh the benefits of selling your house.

Experts Forecast a Turnaround in the Housing Market in 2023

Experts Forecast a Turnaround in the Housing Market in 2023

The housing market has gone through a lot of change recently, and much of that was a result of how quickly mortgage rates rose last year.

Now, as we move through 2023, there are signs things are finally going to turn around. Home price appreciation is slowing from the recent frenzy, mortgage rates are coming down, inflation is easing, and overall market activity is starting to pick up. All of that’s great news for the housing market this year. Here’s what experts are saying.

Cristian deRitis, Deputy Chief Economist, Moody’s Analytics:

“The current state of the housing market is that it is certainly in transition.”

Susan Wachter, Professor of Real Estate and Finance, University of Pennsylvania’s Wharton School:

“Housing is going to ease up. I think 2023 will be a turnaround year.”

Lawrence Yun, Chief Economist, National Association of Realtors (NAR):

“Mortgage rates have fallen in the recent past weeks, so I’m very hopeful that the worst in home sales is probably coming to an end.”

Robert Dietz, Chief Economist and Senior Vice President, National Association of Home Builders (NAHB):

“. . . it appears a turning point for housing lies ahead. In the coming quarters, single-family home building will rise off of cycle lows as mortgage rates are expected to trend lower and boost housing affordability.”

Bottom Line

If you’re thinking about making a move this year, a turnaround in the housing market could be exactly what you’ve been waiting for. Let’s connect to talk about the latest trends in our area.

Lower Mortgage Rates Are Bringing Buyers Back to the Market

Lower Mortgage Rates Are Bringing Buyers Back to the Market

As mortgage rates rose last year, activity in the housing market slowed down. And as a result, homes started seeing fewer offers and stayed on the market longer. That meant some homeowners decided to press pause on selling.

Now, however, rates are beginning to come down—and buyers are starting to reenter the market. In fact, the latest data from the Mortgage Bankers Association (MBA) shows mortgage applications increased last week by 7% compared to the week before.

So, if you’ve been planning to sell your house but you’re unsure if there will be anyone to buy it, this shift in the market could be your chance. Here’s what experts are saying about buyers returning to the market as we approach spring.

Mike Fratantoni, SVP and Chief Economist, MBA:

“Mortgage rates are now at their lowest level since September 2022, and about a percentage point below the peak mortgage rate last fall. As we enter the beginning of the spring buying season, lower mortgage rates and more homes on the market will help affordability for first-time homebuyers.”

Lawrence Yun, Chief Economist, National Association of Realtors (NAR):

“The upcoming months should see a return of buyers, as mortgage rates appear to have already peaked and have been coming down since mid-November.”

Thomas LaSalvia, Senior Economist, Moody’s Analytics:

“We expect the labor market to remain robust, wages to continue to rise—maybe not at the pace that they did during the pandemic, but that will open up some opportunity for folks to enter homeownership as interest rates stabilize a bit.”

Sam Khater, Chief Economist, Freddie Mac:

“Homebuyers are waiting for rates to decrease more significantly, and when they do, a strong job market and a large demographic tailwind of Millennial renters will provide support to the purchase market.”

Bottom Line

If you’ve been thinking about making a move, now’s the time to get your house ready to sell. Let’s connect so you can learn about buyer demand in our area the best time to put your house on the market.

Where Will You Go If You Sell? You Have Options.

Where Will You Go If You Sell? You Have Options.

There are plenty of good reasons you might be ready to move. No matter your motivations, before you list your current house, you need to consider where you’ll go next.

In today’s market, it makes sense to explore all your options. That includes both homes that have been lived in before as well as newly built ones. To help you decide which is right for you, let’s compare the benefits of each. Regardless of which option you choose to explore, working with a trusted real estate professional throughout the process is essential.

The Benefits of Newly Built Homes

First, let’s look at the benefits of purchasing a newly constructed home. With a brand-new house, you’ll be able to:

1. Build your dream home

If you build a home from the ground up, you’ll have the option to select the custom features you want, including appliances, finishes, landscaping, layout, and more. Bankrate puts it like this:

“Building means customizing. . . . instead of wishing your home had a certain kind of flooring, a sunroom or some other special amenity, you’ll be able to tailor the property to your exact needs. You also won’t be limited to a specific location or neighborhood.”

2. Take advantage of builder concessions

In today’s market, a lot of home builders are working hard to sell their current inventory before they add more to their mix. That means many of them are offering concessions and are more willing to negotiate with buyers. That could work to your advantage in the process.

3. Minimize home repairs

Many builders offer a warranty, so you’ll have peace of mind on unlikely repairs. Plus, you won’t have as many little improvement projects to tackle. As realtor.com says:

“. . . if something goes wrong with your new home, not only are there likely some manufacturer warranties in place, but many builders also include additional home warranties . . .”

4. Take advantage of energy efficiency

When building a home, you can choose brand-new, energy-efficient options to help lower your utility costs, protect the environment, and reduce your carbon footprint.

The Benefits of Existing Homes

Now, let’s compare those to the perks that come with buying an existing home. With a pre-existing home, you can:

1. Explore a wider variety of home styles and floorplans

With decades of homes to choose from, you’ll have a broader range of floorplans and designs available.

2. Appreciate that lived-in charm

The character of older homes is hard to reproduce. If you value timeless craftsmanship or design elements, you may prefer an existing home.

3. Join an established neighborhood

Existing homes give you the option to get to know the neighborhood, community, or traffic patterns before you commit. Plus, they have more developed landscaping and trees, which can give you additional privacy and curb appeal.

4. Move in faster

If you have a short timeframe to move or you just don’t want the process to take several months while your home is under construction, buying an existing home might make sense for you. U.S. News explains:

“When you’re choosing a home, existing or new, you should also consider how long it might take to move into that home. Just because you have a contract doesn’t mean that your new home will be completed (or even started) at the time you agree to the purchase. It can be a struggle waiting for the walls to go up as you wonder what your home will become.”

When thinking about where you’ll go after you sell your house, remember your options. As you start your search, think about what’s most important to you. By working with a trusted real estate agent, you can be confident you’re making the most educated, informed decision.

Bottom Line

If you have questions about the options in our area, let’s discuss what’s available and what’s right for you, so you’re ready to make your next move with confidence.

Why It Makes Sense To Move Before Spring

Why It Makes Sense To Move Before Spring

Spring is usually the busiest season in the housing market. Many buyers wait until then to make their move, believing it’s the best time to find a home. However, that isn’t always the case when you factor in the competition you could face with other buyers at that time of year. If you’re ready to buy a home, here’s why it makes sense to move before the spring market picks up.

Spring Should Bring a Wave of Buyers to the Market

In most years, the housing market goes through predictable seasonal trends in activity. Winter is typically a quiet point in the year, while spring sees a surge of buyers begin their search. And experts project that this year will be no exception.

Right now, buyer demand is low due to a combination of normal seasonal trends and a reaction to last year’s rise in mortgage rates. But rates have started to come down since last November, which has more and more potential buyers planning to jump into the market. That means right now is a sweet spot if you’re in a good position to buy, before more buyers reappear. Affordability is beginning to improve, but demand is still low — for now. Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), shares:

“. . . expect sales to pick up again soon since mortgage rates have markedly declined after peaking late last year.”

If you’re ready to buy a home, right now is the best time to do so before your competition grows and more buyers enter the market.

Today’s Sellers Are Motivated

Low demand from buyers often means sellers are more motivated to work with you, and that can set you up to buy a home on your terms. In fact, sellers have been more willing to negotiate this winter because there are fewer buyers in the market. According to a recent article from Forbes:

“. . . sellers gave concessions to buyers in 41.9% of home sales in the fourth quarter of last year.”

But keep in mind, the advantages buyers have this winter won’t last forever. The competition you face could be greater if you wait until spring to make a move, and increased buyer demand means sellers will have less motivation to negotiate with you. Be sure to work with a trusted real estate professional to learn what you can expect in your local market right now.

Bottom Line

If you’re in a good position to make a move, it may make sense to move before spring. Working with your team of expert real estate advisors is the best way to learn about the current market and what it means for you. Let’s connect today to determine the best plan to achieve your homebuying goals.